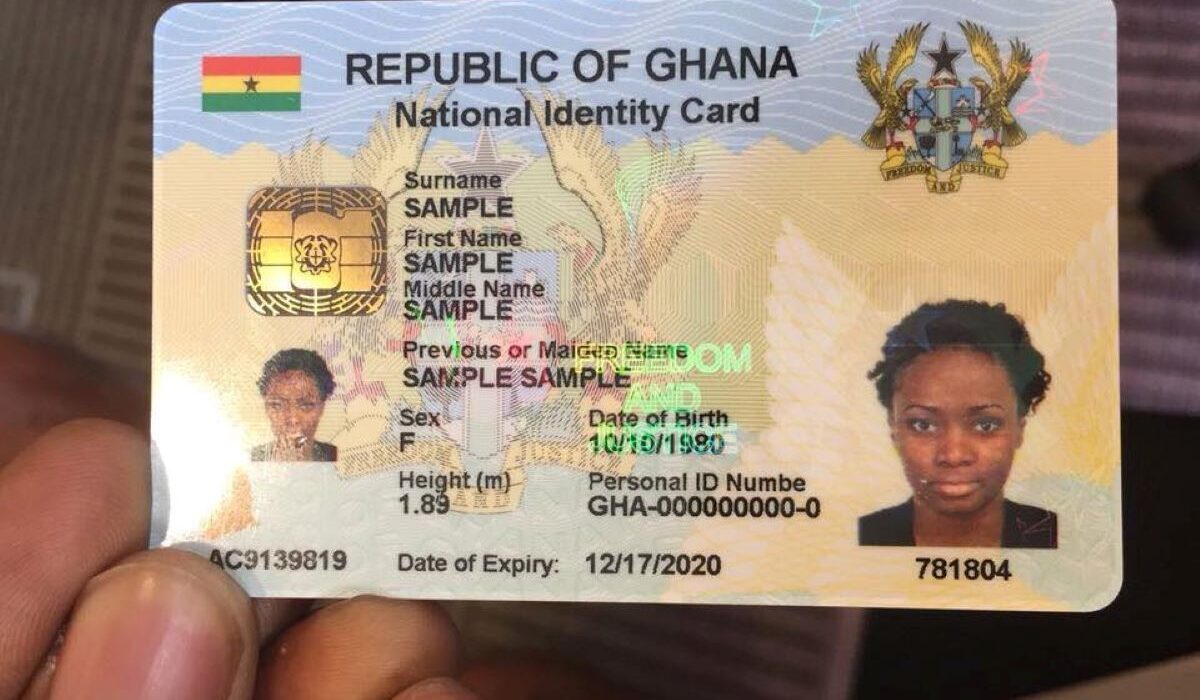

Ghana’s National ID has been upgraded to a payment card as well.

Ghanaians already use the card to register SIM cards, apply for passports, and access government services can now hold money, process payments, and send funds internationally.

The National Identification Authority (NIA), the statutory body that manages Ghana’s national identification system, has activated an e-wallet directly on the Ghana Card. The move has been in the works since at least September 2025, and it is now live.

What is the Ghana Card e-wallet and what can you do with it?

The Ghana Card e-wallet allows cardholders to:

- Withdraw cash from ATMs

- Pay in physical stores and online

- Make international payments to over 200 countries

- Access services including insurance and emergency assistance

It functions like a debit card, except the card is your national ID. No separate bank card is needed.

How to activate the Ghana Card e-wallet: Existing Ghana Card holders can activate the wallet in one of two ways — through the MyCitizens App or by dialling *402# on their mobile phone.

The card was always designed for this

The NIA has described the Ghana Card as a triple-purpose document from the beginning; identity, passport, and payment. The e-ID has been in use for years. In 2022, the e-passport feature was activated, making the Ghana Card accepted as a travel document in 197 countries worldwide. The e-wallet is the third and final layer.

What sets this apart from mobile money is how it is structured. Rather than being controlled by a single bank or financial institution, the NIA has built the wallet as a shared, interoperable platform, meaning all banks can integrate with it. One card works everywhere.

DON’T MISS THIS: Satellite internet: Why Amazon, Starlink, Meta are scrambling for Africa

Why Ghana’s National ID now includes payments

Ghana’s credit card penetration rate stood at just 0.6% in 2024, and was projected to keep declining through 2029. Most Ghanaians who move money digitally do so through mobile money platforms. Formal card-based financial services have remained beyond reach for a large part of the population.

By embedding a payment wallet directly into Ghana’s National ID, the government is attempting to bring financial services to people without asking them to open new accounts, acquire new cards, or navigate the banking system from scratch. If you have a Ghana Card, and millions of Ghanaians do, you are already enrolled.

Gold trading is next

The NIA has signalled interest in extending the wallet’s use beyond everyday payments. It is in discussions with the Ghana Gold Board, the country’s sole authority for gold trading and export, to make the Ghana Card a platform for gold transactions and tokenised trading. It is not yet confirmed whether that integration is active.

Is Ghana the first African country to add a payment wallet to its national ID?

This claim has circulated widely, but the full picture is more nuanced. Ethiopia launched FaydaPass in 2025, a digital wallet linked to its national ID. And countries including Benin and Djibouti have announced similar initiatives.

Ghana is not operating in isolation. What Ghana has done is move from announcement to activation on a nationally-issued physical card that is already in wide circulation, with a clear interoperability architecture across its banking sector.

Whether it is strictly first depends on how the model is defined, but it is undeniably among the earliest and most developed on the continent.

The broader race to anchor payments in national identity infrastructure, bypassing traditional card networks like Visa and Mastercard, is already underway across Africa. Ghana has made its move.

What this could mean for Africa

If Ghana’s model works at scale, it offers a blueprint other African governments will watch closely. A payment system built on identity rather than on imported card infrastructure could reduce dependency on global payment networks, lower transaction costs, and bring formal financial services to populations that have historically been locked out.

Malawi has already announced plans for a similar system by 2026. The continent is moving in one direction.